Purchasing a house includes a chain of decisions that can affect your life for quite a long time or even decades. The choice to lease or purchase a house is the first. When that is ruled out in favor of ‘purchase’, discovering the ideal home for your family is the next step. And afterward comes the critical ‘Fixed or Floating Rate Interest’ home loan choice. This choice affects your bank balance and subsequently, requires cautious consideration. So what’s the difference between the two and which is more favorable for you?

Let us find out which choice is better: Fixed home loan or Floating home loan

You can opt for a floating home loan interest rate if –

Expecting the interest rates to fall

Uncertain about interest rate movements

Looking for a few investment funds on your interest rate in the near term

You can opt for a fixed home loan interest rate if –

Okay with the EMI you are resolving to pay

Anticipating interest rates to increase

If interest rates have descended, you hope to secure at that rate

In case you are not capable to make your mind up, opt for a group loan – fixed and floating home loan interest rate in half-half.

You can swap between a fixed and floating home loan interest rate at a minimal fee.

It is very important to focus on the home loan’s interest rate because it is the interest rate that determines affordability. Besides the home loan interest rate, likewise, consider the type of interest that you pick. You can pick between a fixed and floating home loan interest rate accordingly.

Floating and fixed home loan interest rates, both have their own benefits. Thus, it is important that you understand the meaning of both the home loan interest rate and its benefits and then act accordingly.

About fixed home loan interest rate and its benefits

Fixed home loan interest rate implies to reimbursement of home loans in fixed equivalent portions over the entire time-frame of the loan. For this situation, the loan fee doesn’t change with market variances. Near the beginning part of the loan tenure, most of the scheduled monthly installments are utilized to support the interest and the principal is paid in the latter part of the term.

Benefitsof Fixed home loan interest rate

Interest rate is fixed regardless of market variances

A fixed home loan interest rate is brilliant for the individuals who are skilled at budgeting and want a fixed month-to-month reimbursement plan, which is anything but difficult to spending plan and doesn’t vacillate.

It gives a feeling of sureness and security

About floating home loan interest rate and its benefits

Floating home loan interest rates by name infers that the rate of premium differs with economic situations. In this home loan, the interest rate is fixed to a base rate in addition to a floating factor thereof. Therefore, if the base rate fluctuates the floating interest rate fluctuates as well.

Benefitsof Floating home loan interest rate

The prime benefit of floating home loan interest rates is that they are less expensive than fixed home loan interest rates. Therefore, in case that you are getting a floating home loan interest rate of 11.5 percent while the fixed home loan interest rate is being proposed at 14 percent, yet you set aside money in case the floating loan interest rate increases up to 2.5 percent.

Though floating home loan interest rate goes more than the fixed interest rate, it will be for some time of the loan and not the whole term. The interest rates will undoubtedly fall over an extensive stretch and, subsequently, the floating home loan interest rate brings plenty of investment funds.

Despite everything, you can’t choose?

If you are not yet certain about which home loan you should prefer, settle on a group loan – half fixed and half floating. This is particularly reasonable for you in case you have other loan reimbursements at the moment and your incomes have been premeditated to meet your loan commitments for the initial 3-5 years; during this term, you can pick a fixed interest rate home loan. After this stage, you can go for a floating interest rate home loan for the remaining tenure of the loan.

To finish up, one cannot state that one loan type is superior to the next; choosing the fixed or floating home loan interest rate will purely rely upon your requirements, priority and economic condition.

Meanwhile, consider the above-mentioned factors to choose the alternative that suits you best. Moreover, you can contact Protech Group for more details on home loans and real estate rates.

Since time immemorial, the land has never lost the value or demand, and with just restricted space accessible for a quick expanding populace, realty offers better (and ensured) returns contrasted with other well-known investment decisions. Protech Group of Real Estate Company in Guwahati prefers choosing location best suited from a flat buyer’s perspective.

India maintains to hang on to its position as the world’s fastest developing significant economy with the help of improved shareholder conviction and better policy amendments. The IMF’s (International Monetary Fund) database furthermore suggested that India’s obligation to world development has extended from 7.6% during 2000-2008 to 14.5% in 2018.

Let’s check out the 2019 real estate market

Flats are cheaper: Many metropolis saw prices fall. In others, the price upsurge was lower than the buyer value rise. Excluding Hyderabad, prices were down in genuine terms all over India.

Lower GST rate: Decreasing the GST rate to 1% for reasonable accommodation and 5% for others improved purchaser acuity. Be that as it may, developers scaled costs to counterbalance for the loss of input tax credit.

Impact of rate cuts: Rate cuts by the RBI have relieved yet not to the degree they ought to have. The repo rate was cut by 75 bps but only around 35 bps cut was passed on to borrowers.

Investors are out: Due to the high cost of capital and a moderate rise in prices, investors are keeping away from real estate. Purchasers rather opted for ready-to-move-in flats than under-construction apartments.

Builders play safe: After the introduction of the RERA, builders are being careful not to take any risks. Relatively few new projects were being launched. Rather, builders focused on completing their ongoing projects. Protech group real estate companies who are also RERA approved builders in Guwahati launched only one project, Protech warehouse Bongora, as the company believes in providing quality rather quantity.

Property value has fallen to some extent: Massive inventories and strict regulations have kept property value low crosswise over significant Indian urban areas, according to the most recent report for most of 2019. Protech Group provided subsidy loans under PMAY to ease property buyers in Guwahati. Protech galaxy, Bhetapara is the ongoing residential project and the sale is still on.

Innovative offerings by Builders: real estate builders have made every possible effort to enhance by offering theme-based projects to homebuyers like – comfort homes with branded amenities like senior citizen resting area, kid-friendly playground, infinity pool, and much more.

Protech’s upcoming project, Protech Akansha is also a theme-focussed residential project designed to provide the most branded amenities at an affordable price.

We could see that 2019 has been a year that proved neither too providential nor too untoward for the real estate sector or homebuyers. So, with this year almost at the edge of closing, let’s move onward the new year with a good note- “New Year, New Day, New Beginning.”

Guwahati is the best place to buy a flat in Assam.

Guwahati is a budding city, popularly known as the temple city, and is surrounded by hills. There is a hill view from almost anywhere, stand in a crossroad and you can view a hill in front of you. The gateway to other North-eastern states with frequent and good transportation facilities: This is one of the most eminent points which makes Guwahati the best place to buy a flat.

Moreover, most of the real estate builders in Guwahati are approved by RERA and apartments are designed according to the guidelines of Pradhan Mantri Awas Yojana which facilitates the buyers to reap benefits of purchasing flats at subsidized rates. Protech Group is an award-winning real estate builders in Guwahati, and also approved by RERA. If you are planning to buy a flat in Guwahati, the sale is on in Protech Galaxy.

Guwahati is a good place to shift to for people planning to move from other metro cities or states. Little setbacks are congestion on streets and exigency of good jobs despite higher educational institutes like the IIT Guwahati, Royal Global Institute, etc. However, if you plan well ahead of buying a flat in Guwahati, the change from other metro cities can be very cost-effective and the cosmopolitan city will not be taken away from your active lifestyle as well.

These are a few focal points that make Guwahati the best place to buy a flat:

A designated smart city with a domestic and international airport, and metro being planned.

Moderate pollution levels as compared to other metros.

Lower cost of living and affordable property.

Centre point of the North East states with good connectivity, and frequent transportation facilities.

Considering the above-mentioned points Guwahati sounds a great place to invest in a house. However, a good location can mean different things to different people, of course, but there are also objective factors that determine a home’s value. Depending on your personal needs and preferences, you may not be able to buy a home with all of these factors. That’s okay – beyond everything, a home is much more than just an investment. But, next time you are purchasing a new flat in Guwahati, keep the following factors in mind.

1. Centrality

Where you choose to live in a city or town will undoubtedly affect how much you pay for your home. The land is a finite commodity, so cities like Mumbai and Delhi are highly developed and don’t have a lot of room for additional growth, tend to have lofty costs than cities that have too much room to expand, which is an exception in Guwahati till date.

2. Neighborhood

While choosing a buy an apartment, neighborhoods that fascinate you will mostly be an affair of personal choice. However, a truly good neighborhood will have a few key factors: appearance, accessibility, and amenities.

Appearance: Large trees, landscaping, and nearby green or community spaces tend to be desirable. You can also judge the popularity of the neighborhood based on how long homes in that area tend to stay on the market; if turnover is quick, you are not the only one who thinks this is a desirable place to live.

Accessibility: a neighborhood that is situated near your city’s major routes and that has more than one point of entry. Commuting to and from work is a big part of many people’s day, so a house with easy access to roads and/or public transportation will be more desirable than one that is far and can only be accessed by one route.

Amenities: Important amenities such as grocery stores, shops, and restaurants are what most buyers look for while choosing a location to buy a flat. Most people like places that are well-situated – in case you have to go a long distance to get to anything; it’s likely to make your house less attractive. Schools are another important amenity – even if you don’t have kids, if you want to sell your home in the future, many buyers will be on the lookout for good schools.

Protech builders consider all the necessary points and develop structures that suit the tastes and requirements of homebuyers in Guwahati.

3. Development

While deciding on property purchase it’s not just existing amenities that matter, but future ones as well. Plans for schools, hospitals, public transportation, and other commercial infrastructure can significantly pick up property values in the area. When you are buying a home, try finding out if any new public, residential, or commercial developments are planned and take into account how these add-ons might have an effect on the suitability of the adjacent areas.

People from Guwahati as well as also outside the city have a magnificent prospect to invest here in Guwahati nestled amidst fresh air, far from the maddening crowd, yet close to all essential civic amenities. We, the Protech Group of builders think from our customer’s perspective and deliver the best suitable projects to cater to their needs. Have a look at our current project https://bit.ly/2PJ2rIf, you never know, your dream home might be just at a click away!

Purchasing a house in Guwahati or anywhere on earth is not an easy job. As though saving money to own a dream house isn’t arduous enough, you need to really focus to choose what to purchase. You decided to buy a flat, chose the locality, and financially ready and had talked about with your family. This certainly looks like you are on the right track. But, since you are investing a big amount you would prefer not to commit any error in a rush. Isn’t that so?

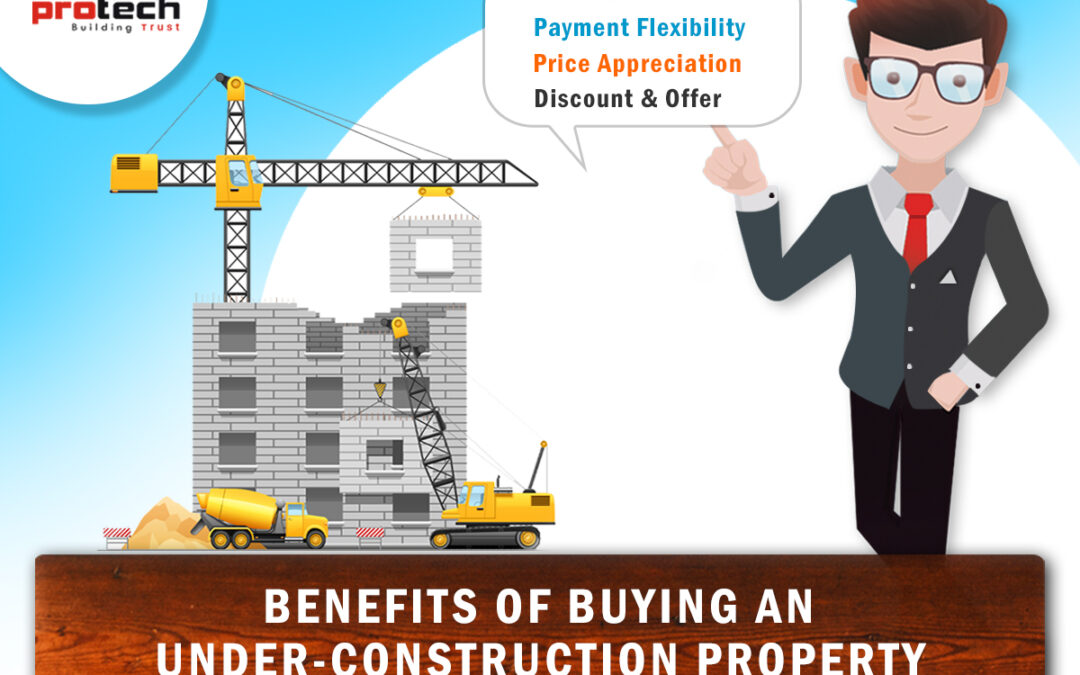

There are basically two options while buying a flat- Ready-to-move-in flat and an Under-Construction flat.

Thus, the major confusion that starts while planning to buy a flat is which type of flat to purchase a flat which is under construction or the one which is ready-to-move-in?

For many property buyers, ready-to-move-in projects sound the most appropriate investment. However, underdevelopment projects are no less as far as quality and cost are concerned. In case you execute meticulous research on the project, location, value, engineer, and other related perspectives; the under-construction flats provide a positive reception than ready-to-move-in flats.

Benefits of under-construction property

Low cost

The cost of under-construction flats usually starts at a low price. As the demand increase when more people start purchasing, the market cost shoots up.

As a buyer, if you invest early you can benefit from the price movement. But, you need to carefully find a builder with a track record of completing projects on time.

As a purchaser, the sooner you invest the best price benefit you get. However, you have to cautiously discover a builder with a reputation for finishing projects on schedule.

Real Estate Regulatory Act 2016 (RERA) has made it is mandatory to register every under construction property where land is above 500 Sq./8 number apartments. This act seeks to protect buyers from any kind of real estate frauds and scams. People planning to purchase a flat or an apartment can be more confident about under-construction projects, as builders are legally obliged to register to provide better transparency in project marketing and implementation.

Failing to do so, the builder shall pay a penalty to the homebuyer and the government.

Payment Flexibility

Many builders offer payment flexibility for under-construction properties.

One of the best benefits of buying an under-construction-flat is payment flexibility.

A lot of builders will offer you payment options where you can pay a lump-sum amount and book your apartment in an under-construction building and EMI would start after you get ownership. Thus, the extra time gives you more time to orchestrate the additional sum required for registration and diverse incidental expenses.

Price Appreciation

Contingent on the location, infrastructure, connectivity, future possibilities you can anticipate price appreciation in the under-construction flat between 8 should 16 %.

To get the best return of profitability, you should check the past information on property costs in the close proximity. You can otherwise get in touch with resident property counsel to get a fair idea of the market.

Customization

Starting from the floor to the roof, bedroom to bathroom, kitchen to a balcony, you can customize and get a home built according to your choice in case you settle for an under-construction apartment. Protech Group offers exciting prices on under-construction flats in Guwahati along with customization benefits.

However, it’s not the case if you opt to buy ready-to-move-in flat then you will have no option left for customizing but have to move-in an already built house according to the builders’ designs and dimensions.

Discount & Offer

To draw the attention of new purchasers many builders offer alluring offers like discounts and lucky draw. Why not try your luck and own the house you always dreamt of? In under-development property, you will moreover, have the option to pick the floor number, which direction the house faces depending upon availability.

Conclusion

Protech is a RERA certified real estate company. We are committed to on-time project delivery and customer is the King for us. Moreover, our projects are built under strict standards of technology design and we deliver quality flats at the best price. Check Out our ongoing project, Protech Galaxy https://bit.ly/2DOM0DC

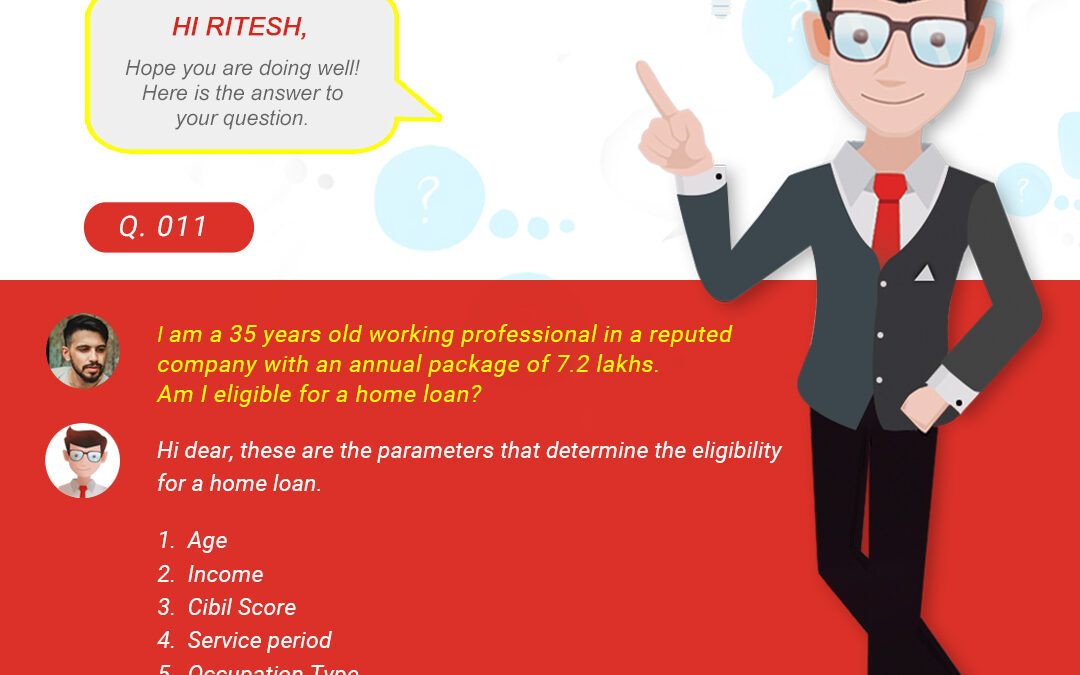

Loan eligibility depends primarily on income, in case a borrower doesn’t know about the particular standards that go into calculating that eligibility. If the applicant could not meet the eligibility criteria may prompt refusal of the loan application, leaving a negative imprint on the person’s credit profile.

If a person applying for a loan requires a clear idea of the parameters that are considered, they can seek help from the nearest bank or can visit their website to check. The loan lender will inspect the applicant’s income documents, credit history, CIBIL score, age, and related parameters.

Below are the 5 major parameters that determine the eligibility criteria of the borrower to avail a home loan:

1) Age

2) Income

3) Cibil Score

4) Service period

5) Occupation Type

Home loan eligibility based on age

Age is one of the most prominent determining factors when it comes to loan tenure. The maximum tenure that you can benefit is 20 years.

You will be able to avail of a longer repayment tenor if you are of a lower age. You can also avail of a home loan of higher value provided you have a high income.

You will have the option to benefit a longer repayment period in case you are younger. You can likewise benefit a home credit of higher worth gave you have high pay.

Salaried applicants have to be between the ages of 23 and 62 years to apply for a home loan. Self-employed applicants have to be within the age bracket of 25 and 70 years to avail one.

The table below explains the maximum tenure a person is eligible for based on their age:

Age

Salaried applicants – Maximum tenure

Self-employed applicants – Maximum tenure

25 Years

30 years

30 years

30 Years

30 years

30 years

35 Years

30 years

30 years

40 Years

30 years

30 years

45 Years

25 years

25 years

45 Years

20 years

20 years

Home loan eligibility based on income

Another parameter that determines the eligibility criteria of how much loan an individual can avail is the income (in-hand salary). Income is important as it assists in calculating a borrower’s repayment potential.

An individual’s salary will decide the credit sum you are qualified for. Banks will consider your in-hand salary, minus a few general deductions, for example, PF, ESI, gratuity, etc. The in-hand income will decide the EMI sum you can manage the cost of and consequently the total amount of loan one will get.

For example, if the in-hand monthly salary is Rs. 25,000, an applicant can borrow as much as Rs.18.65 Lakh as a loan to buy or build a home worth Rs. 40 Lakh (if there are no current monetary commitments.) But in case the monthly in-hand income is Rs. 50,000, you can get Rs. 37.28 Lakh for the same property. Similarly, if the take-home is Rs. 75,000 an applicant can increase the loan amount to Rs. 55.93 Lakh.

Age

Net monthly income (in Rs.)

25,000

50,000

75,000

25 Years

18.64 Lakh

37.28 Lakh

55.93 Lakh

30 Years

18.64 Lakh

37.28 Lakh

55.93 Lakh

35 Years

18.64 Lakh

37.28 Lakh

55.93 Lakh

40 Years

18.64 Lakh

37.28 Lakh

55.93 Lakh

45 Years

18.64 Lakh

37.28 Lakh

55.93 Lakh

50 Years

18.64 Lakh

37.28 Lakh

55.93 Lakh

Home loan based on Cibil Score

What CIBIL Score?

A CIBIL score is a three-digit number sum up of a borrower’s complete loan history. The value of a credit score is normally between 300- 900. The loan applicant’s CIBIL score is prepared based on their credit history. This comprises all verified as well as unbound loans and whatever other obligations that you may have or had.

It is good to always know one’s CIBIL or credit score before applying for a loan. One can get their credit report from CIBIL by paying a nominal fee. A credit report will consist of the below records:

credit benefited by the borrower

repaying loans and credit card bills

delayed payments or failure on past credit held by you

credit cards and loans that you currently hold

fresh information about loan and credit card applications submitted by the borrower

Higher the CIBIL score, the greater the chances to get a loan. A higher CIBIL score means that the individual is financially sound and has reimbursed each commitment on time. But, a lower score doesn’t really imply that the individual has not paid his/her duty on time. A new borrower may have even a zero CIBIL rating. The base CIBIL score for home loan approval is 750. Moneylenders look at the CIBIL score to decide if a person is eligible for a home credit. They inspect credit inquiry to check the same. Apart from that, a few banks may offer a home loan against a lower rating since these credits are secure.

Home loan based on Service period

The service period plays an important role in determining the eligibility for a home loan. Service period clarifies the stability of a borrower besides, in determining the capability of loan repayment.

A bank will not give loan to a person who has just started working or is under probation period. The bank will also not provide a home loan to a person who is working on a contractual basis.

Moreover, the service period to be served will be also looked upon while determining eligibility for a home loan. If a person is already in his or her 50s or 55+ and let’s say, the loan tenure is for the next 20 years. In such cases also, the possibility of getting a home loan is less to no.

Example: A person goes for a home loan of Rs. 15, 00,000 over a period of 20 years. Let’s say, the building will be completed in 3 years, during which this person thinks to pay pre-EMI. Following the completion of these 3 years and the pre-EMI payment termination, the EMI reimbursement period begins. Subsequently, the total loan tenure would be 3 years (pre-EMI period) + 20 years (loan tenure) = 23 years.

Thus, a salaried individual should have at least two years of work experience, and not more than 50 years of age in order to be eligible for a home loan. In the case of self-employed individuals, the business should run for at least 3 years.

Home loan based on Occupation type

Another important parameter to be eligible for a home loan is the occupation type. A person working in any organization must be working on a permanent post not on a project or contract basis to get a home loan.

Moreover, banks give preferences based on the type of organizations an applicant works. For example, if a salaried person is working in Navaratna companies like ONGC and OIL or in MNCs like HP, Infosys, etc. eligibility to get a home loan is more in such cases.